Supplemental insurance can fill gaps left by core policies, but it often requires periodic tuning to remain effective and affordable. Small, practical adjustments can reduce out-of-pocket costs while preserving access to preferred providers and services. This article outlines clear actions you can take to evaluate and strengthen supplemental coverage without unnecessary complexity. Follow these steps to create a manageable review routine that keeps your plan aligned with changing health and financial needs.

Evaluate Your Current Coverage

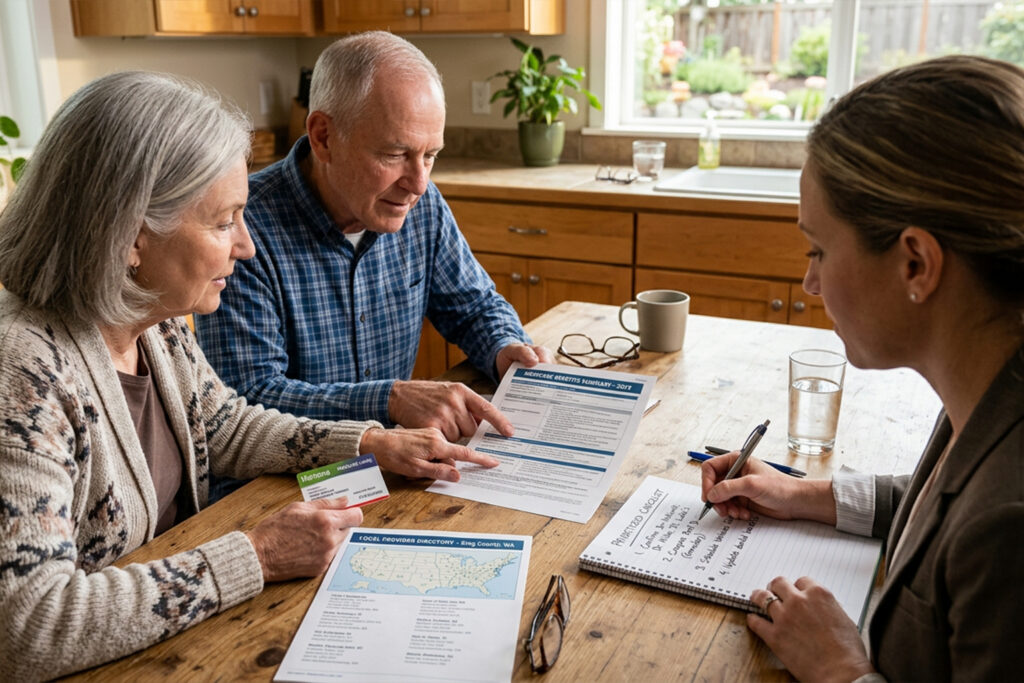

Begin by listing existing benefits, deductibles, copays, and any annual limits that apply. Compare what you actually used last year against what your policies cover to spot gaps or redundancies. Pay particular attention to services that generated unexpected bills, such as specialist visits or durable medical equipment. This baseline makes it easier to prioritize changes and avoid paying for overlapping coverage.

Documenting claims and recent medical needs also clarifies whether to increase, reduce, or shift benefits. A clear inventory saves time when comparing alternatives and prevents surprises during renewal periods.

Prioritize Benefits Based on Your Needs

Identify which benefits matter most given your health profile and lifestyle, such as prescription drug support, dental, vision, or home health aides. Rank potential gaps by frequency of use and potential financial impact to decide where coverage will do the most good. Considering future needs helps avoid frequent plan changes that can be costly or confusing. Prioritization helps you focus on value rather than features that look attractive but offer little real benefit.

- Prescription coverage for ongoing medications

- Outpatient and specialist cost sharing

- Support for long-term or home-based care

With priorities set, you can seek plans that bolster the most important areas while accepting lower coverage where risk is smaller. This approach keeps premiums targeted and efficient.

Compare Costs and Provider Networks

Review total expected costs, not just monthly premiums: include deductibles, copays, coinsurance, and annual maximums. Check whether preferred doctors and local facilities are in-network to avoid elevated out-of-pocket charges. Use summary of benefits documents to perform side-by-side comparisons and watch for hidden limits on commonly used services. Remember that small differences in cost-sharing can add up across multiple visits and procedures.

Choosing a slightly higher premium with broader network access can be cheaper overall if it prevents frequent out-of-network fees. Verify network updates annually since provider participation can change.

Use Tools and Professional Advice

Leverage online comparison tools offered by independent marketplaces or consumer groups to filter plans by cost, benefits, and network coverage. Meet with a licensed advisor or a trusted counselor for a personalized review if your situation is complex. Advisors can spot clauses and riders that matter and explain trade-offs in plain language. Keep documentation of recommendations and expected outcomes for future reference.

When seeking advice, choose unbiased sources and confirm credentials to avoid conflicts of interest. A second opinion can also highlight alternatives you may have missed.

Plan for Changes and Review Regularly

Set a calendar reminder to review supplemental coverage annually or after any major life or health change. Reassess priorities if medications, mobility, or care needs shift, and update beneficiaries and contact details accordingly. Even if premiums are stable, benefit changes or network adjustments may require action. Regular reviews make renewals deliberate rather than reactive.

Scheduling reviews around open enrollment periods ensures you can make timely changes without gaps in protection. A short annual check keeps coverage aligned and budget-friendly.

Conclusion

Regular, focused reviews of supplemental insurance help seniors control costs while preserving important benefits. By evaluating coverage, prioritizing needs, comparing options, and consulting credible resources, you can make informed adjustments. Small, planned actions each year keep protection responsive to changing circumstances.