Improving your credit score is less about dramatic moves and more about consistent, measurable planning. Small adjustments in how you manage payments, balances, and account openings can compound into meaningful gains over months. This article outlines practical steps to set targets, optimize routines, and track progress without undue stress. Use these reliable actions to build steadier credit over time.

Set Clear, Realistic Targets

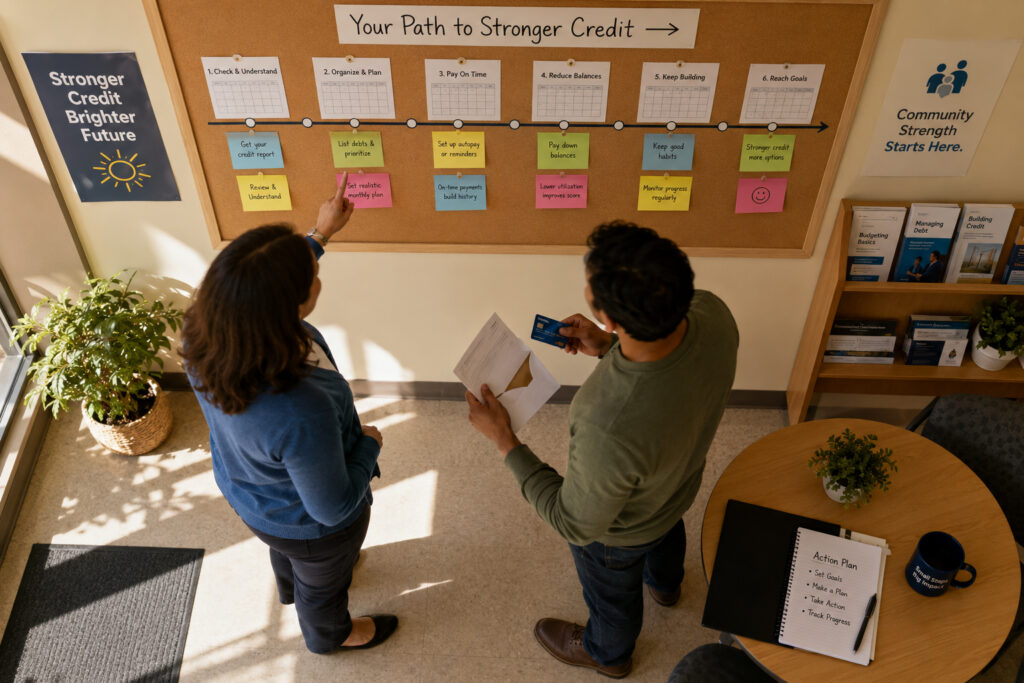

Start by establishing specific, attainable goals for your score and a reasonable timeline for achieving them. Review your credit report to identify the highest-impact areas such as payment history, utilization, and account age, then prioritize actions accordingly. Break big goals into monthly milestones so progress is visible and manageable. Clear targets help you choose daily and monthly behaviors that align with long-term improvement.

Write targets into a simple tracker or budgeting tool and check them each month. This keeps choices deliberate and progress measurable.

Optimize Payment Timing and Amounts

On-time payments are the single most important factor, so automate bills when possible and aim to pay more than the minimum. Consider making one or more mid-cycle payments to lower the balance that gets reported at statement close. Reducing reported utilization is often faster than paying off a balance completely and can raise scores within a few cycles. Small, regular overpayments also reduce interest and shorten payoff time.

Automation reduces late payments and stress, while strategic extra payments accelerate improvement. These adjustments are simple but effective.

Manage Credit Utilization and Accounts

Lowering credit utilization is a direct way to improve scoring models: pay down high balances and spread charges across cards to reduce ratios. Avoid closing long-standing accounts unless fees or risks outweigh the benefit, since keeping older accounts helps the length-of-history factor. When you need more available credit, request a limit increase rather than opening new accounts, and space any new applications to minimize inquiry impact. Thoughtful account choices protect both capacity and profile health.

- Pay highest-balance cards first to reduce utilization quickly.

- Ask for credit limit increases if your issuer allows without a hard inquiry.

These habits maintain flexibility while improving core metrics that scoring models use. Regular review prevents small issues from growing.

Monitor and Adjust Regularly

Check your credit reports periodically and use monitoring alerts to catch errors or identity issues early. Dispute inaccuracies promptly and follow up until corrections appear; reporting fixes can yield quick benefits. Track progress against your milestones and change tactics based on measurable results, such as increasing payment frequency or shifting balances. Ongoing adjustments turn short-term wins into long-term stability.

Consistent monitoring supports smarter decisions and timely fixes. Over time this discipline builds resilience in your credit profile.

Conclusion

Start with clear targets and small timing changes to build momentum.

Monitor results and adapt your plan as balances and circumstances change.

Small, consistent actions will produce measurable credit improvements over time.