Retirement brings new priorities for health coverage, and planning ahead helps avoid costly surprises. Supplemental plans can fill gaps left by primary policies, but choices differ widely in benefits, costs, and exclusions. This article outlines practical steps to identify gaps, weigh trade-offs, and align coverage with personal needs and budgets. Use these ideas as a structured starting point to make confident, informed decisions.

Identify Coverage Gaps

Begin by listing typical exposures such as outpatient costs, prescription drugs, dental, vision, and long-term care services. Review recent medical bills and any expected care to estimate annual out-of-pocket risk. Look at existing policy summaries to spot limits, waiting periods, and services that are excluded.

Documenting gaps makes comparisons more objective and reveals where supplemental benefits offer the most value. A clear inventory helps avoid paying for redundant coverage while ensuring critical needs are addressed.

Prioritize Needs and Budget

Decide which benefits matter most based on health history, ongoing treatments, and family risk factors. Prioritize must-have protections first, such as prescription drug coverage or skilled nursing benefits, then consider optional add-ons. Balance expected annual costs against premiums to determine a reasonable spending range.

Setting priorities prevents over-insuring in low-risk areas and under-insuring where expenses would be catastrophic. This approach keeps plans affordable while protecting against the most likely financial shocks.

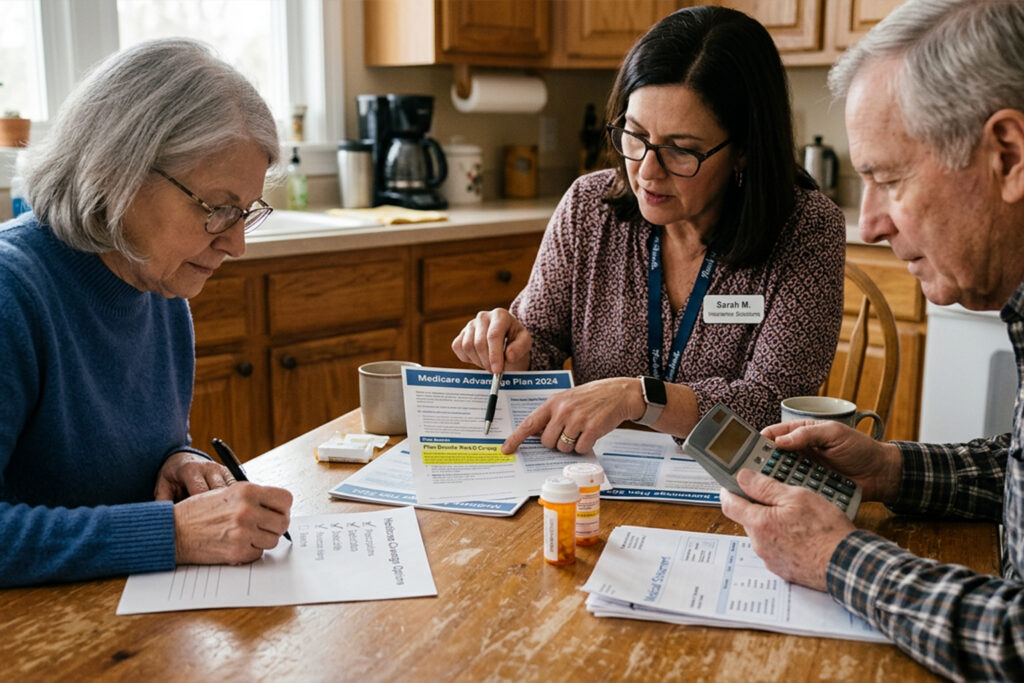

Compare Features and Total Costs

When comparing plans, evaluate more than the headline premium: consider deductibles, co-pays, annual limits, provider networks, and exclusions. Look at lifetime limits and caps on specific services, as these can create unanticipated exposure. Use side-by-side comparisons to spot meaningful differences in real-world scenarios.

- Check provider access and whether favorite doctors are in-network.

- Confirm drug formularies and prior authorization rules.

- Estimate your annual total cost under each plan.

Focusing on comprehensive cost and access measures reveals which plans deliver practical protection rather than just a low monthly price. Realistic scenario testing helps choose the best match.

Enrollment and Ongoing Review

Pick an enrollment window that minimizes gaps and aligns with other benefits changes. Keep documentation of plan details and important dates, and set an annual reminder to reassess coverage. Life changes, new prescriptions, or price shifts can make a previously optimal plan less suitable.

Regular reviews ensure coverage continues to match needs and budget over time. Small adjustments annually can prevent large problems later.

Conclusion

Securing reliable health coverage in retirement starts with a clear assessment of gaps, priorities, and true costs. Compare options against realistic scenarios and schedule yearly reviews to adapt as needs change. Thoughtful, stepwise planning reduces risk and preserves financial peace of mind.