Managing supplemental insurance can feel complex, but small, deliberate actions often prevent costly surprises. This article outlines practical steps seniors and their families can use to review and strengthen coverage without confusion. The focus is on clear priorities, simple comparisons, and lifestyle choices that lower risk. These approaches keep coverage aligned with needs while avoiding unnecessary expense. Small planning steps can be done annually or after major health changes to keep decisions current.

Identify Coverage Gaps

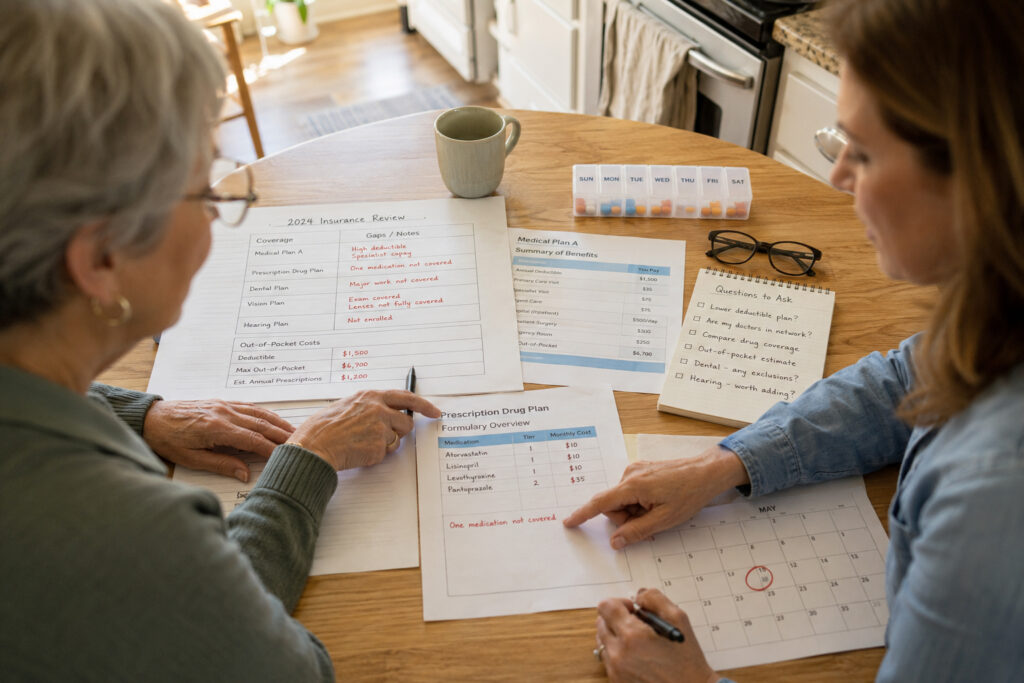

Start by gathering all current policy documents and recent explanation of benefits statements. Look for services that are limited or excluded, such as dental, vision, hearing, or long-term care elements, and note any high out-of-pocket costs. Pay attention to annual limits, provider networks, and pre-authorization requirements that could trigger unexpected bills. Documenting these gaps creates a clear checklist to guide decisions. Include contact numbers and effective dates so conversations are faster when seeking clarification.

A concise inventory of gaps makes follow-up easier with agents or plan representatives. It also helps prioritize which shortfalls should be addressed first.

Compare Costs and Benefits

After identifying gaps, compare the real cost of filling them versus potential out-of-pocket exposure. Estimate annual premiums against likely claims based on your health patterns and projected needs. Consider whether riders, standalone policies, or hybrid products offer better value and bear in mind waiting periods and exclusions. Use comparison tools and ask for written scenarios showing typical claim examples. Be sure to factor in inflation and possible changes to your health status over the coming years when modeling costs.

A cost-versus-benefit approach prevents overbuying coverage that duplicates existing benefits. It also clarifies trade-offs when budget constraints exist.

Use Practical Lifestyle Adjustments

Simple lifestyle choices can reduce reliance on high-cost services and improve negotiating power with insurers. Preventive care, medication reviews, exercise programs, and vision or dental maintenance all lower the frequency and severity of claims. Sharing these routines with your plan administrator can sometimes qualify you for wellness benefits or premium discounts. Small habits accumulate into meaningful savings and resilience. Discuss options with family or caregivers so habits are supported and any coverage adjustments reflect real daily needs.

- Regular checkups and medication reconciliations.

- Routine dental and vision maintenance to avoid costly procedures.

- Participation in approved wellness programs or classes.

Lifestyle adjustments are not a substitute for appropriate coverage, but they meaningfully reduce risk. Combine habits with smart policy choices for best results.

Conclusion

Small, organized steps remove surprises and give seniors more control over insurance outcomes. Regularly reviewing policies, comparing real costs, and adopting preventive habits builds a resilient plan. These actions create peace of mind and a practical financial buffer.