Reviewing supplemental health coverage becomes essential as needs change during retirement. Regularly updating plans helps prevent unexpected costs and ensures access to preferred providers. This article outlines practical actions retirees can take to assess and improve supplemental insurance. The guidance focuses on clarity, affordability, and minimizing gaps in care.

Assess Current Benefits and Identify Gaps

Start by gathering your existing policy documents and a recent summary of benefits from your primary insurer. Compare what is covered versus what you actually use, noting recurring prescriptions, specialist visits, and anticipated procedures. Pay attention to limits, exclusions, and out-of-pocket maximums that could create financial stress. Record any provider network restrictions that might affect continuity of care.

After documenting gaps, prioritize them by potential cost and impact on quality of life. This prioritization will guide which supplemental features are most important to you when shopping. Being methodical at this stage reduces surprises later.

Compare Costs, Coverage, and Provider Access

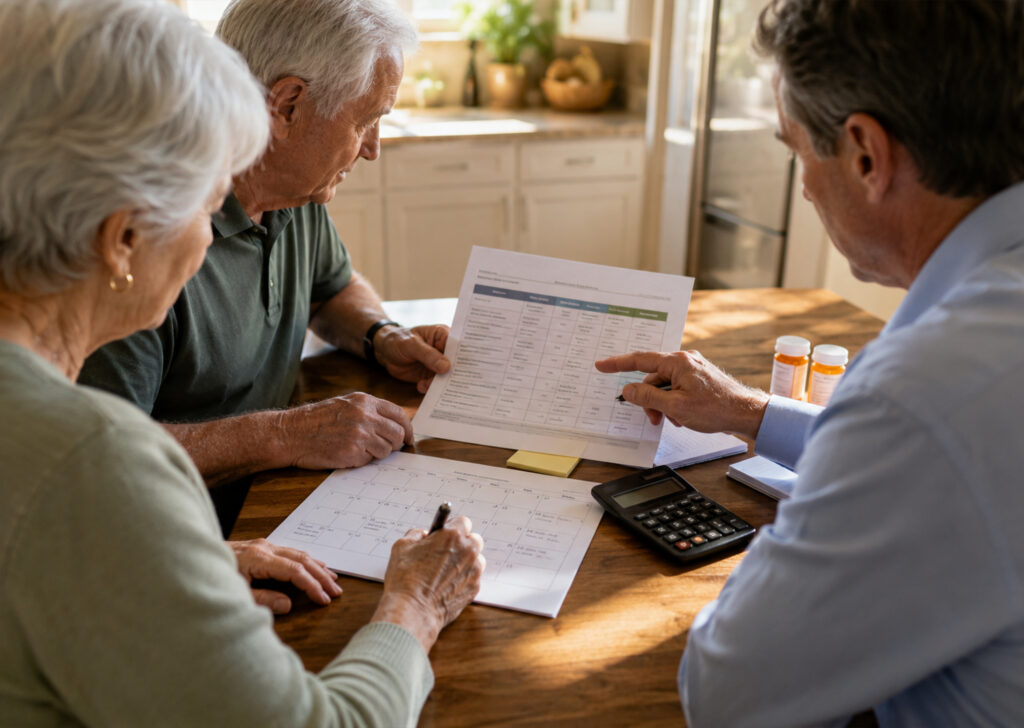

When evaluating options, look beyond premiums to total expected annual costs including deductibles, coinsurance, and copays. Consider whether a plan offers predictable payments for frequent services or better protection for low-probability, high-cost events. Provider networks, prior authorization rules, and pharmacy formularies can materially change the usefulness of a policy. Use side-by-side comparisons and request quotes that reflect your typical care patterns.

- List annual premiums and estimated out-of-pocket spending.

- Check whether preferred specialists and pharmacies are in-network.

- Verify coverage for durable medical equipment or home health if needed.

These concrete comparisons make decisions less emotional and more data-driven. Aim to find plans that balance affordability with the protections you value most.

Timing, Enrollment, and Practical Next Steps

Understand enrollment windows and any penalties for late changes; missing a window can limit choices for a year. If your health or financial situation has shifted, ask whether special enrollment applies and collect documentation if needed. Work with a licensed advisor or plan representative to clarify ambiguous terms and confirm network access. Keep a checklist with renewal dates, contact numbers, and claim appeal procedures.

Finally, set a regular annual review as a habit to capture changes in health, medications, or financial priorities. Small, scheduled updates prevent larger problems down the road and help you stay confident in your coverage.

Conclusion

Updating supplemental health coverage is practical and manageable with a clear process. Focus on documenting needs, comparing real costs, and respecting enrollment timelines. Regular reviews keep protection aligned with changing retirement priorities.