Improving a credit score is a gradual process that rewards consistent habits and informed choices. Many people focus on one metric, but a balanced approach delivers lasting results. This article outlines practical steps you can take to assess your credit, manage accounts, and avoid common pitfalls. Followable routines and small adjustments often produce the biggest gains over time.

Assess Your Current Credit Report

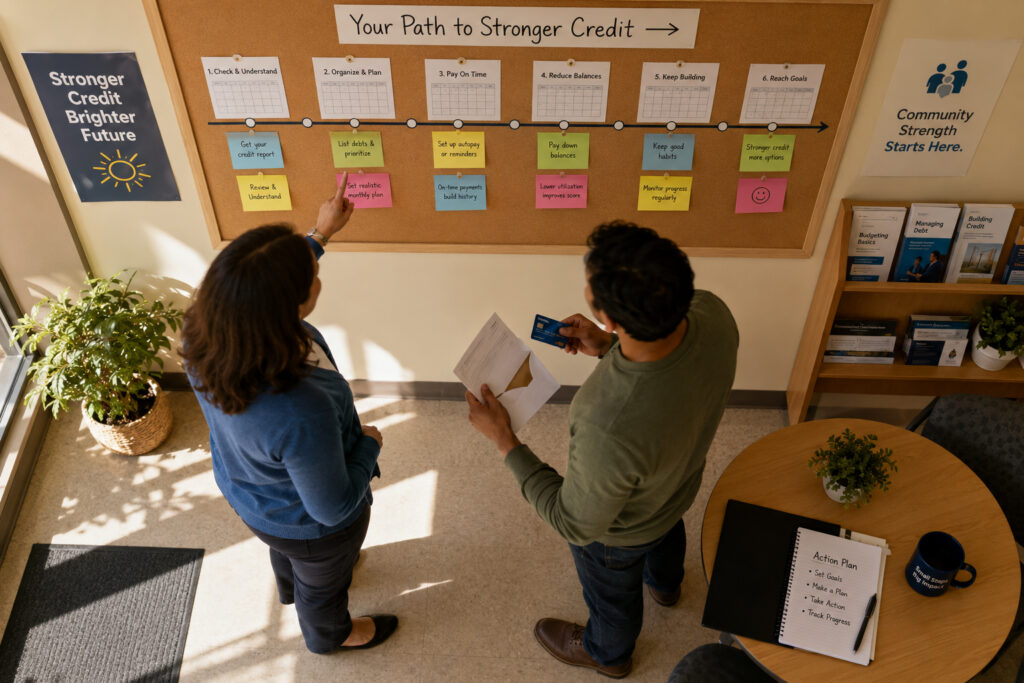

Start by obtaining and reviewing your credit reports from the major bureaus or a reliable monitoring service. Look for errors, unfamiliar accounts, or outdated negative items that could be disputed. Understanding the composition of your score—payment history, utilization, length of credit, new credit, and mix—helps prioritize actions. A clear snapshot makes it easier to set measurable goals and timelines for improvement.

After identifying issues, plan targeted disputes and document communications. Regular reviews every few months help catch changes early and prevent surprises.

Manage Payments and Credit Utilization

Payment history is the single most important factor for most scoring models, so aim to pay at least the minimum on time every month. Setting up automatic payments or calendar reminders reduces missed-payment risk. Credit utilization—the ratio of balances to limits—also has a strong impact, so keep balances low relative to available credit.

- Pay down revolving balances to lower utilization.

- Request higher limits only when necessary and responsibly.

- Use low-interest balance transfer options cautiously to manage debt.

Consistent on-time payments and mindful use of available credit together build momentum toward a higher score.

Build and Protect Healthy Accounts

Maintain a mix of account types without opening unnecessary new credit. Older accounts contribute positively, so avoid closing long-standing cards unless there’s a compelling reason. If you need to add credit, consider a secured card or a credit-builder loan designed for steady reporting.

Protect accounts by monitoring for fraud, using strong passwords, and freezing credit if you suspect identity theft. Responsible behaviors reduce volatility and preserve the gains you’ve worked to achieve.

Conclusion

Improving credit takes patience, consistent payments, and strategic decisions. Focus on reviewing your reports, lowering utilization, and maintaining healthy accounts. Over time these steady habits produce meaningful, sustainable improvements.