Small, consistent actions shape long-term credit outcomes more than occasional big moves. By focusing on simple monthly habits you can rebuild momentum and reduce risk of new setbacks. This article explains practical micro-habits you can adopt without overhauling your finances. Each habit is designed to be measurable, repeatable, and compatible with everyday life. Start with a clear snapshot and layer practices that compound positive effects over time.

Start with a Clear Credit Snapshot

You need regular, objective information before changing behavior. Review your credit reports and scores on a consistent schedule to spot errors, new accounts, or subtle shifts in utilization. Knowing which accounts carry the most balance or which reporting lags exist helps you prioritize actions. This snapshot reduces guesswork and turns vague goals into targeted tasks. It also helps you set realistic timelines for improvement and reduces anxiety.

Set a monthly reminder to review key lines and note any differences. Early detection makes corrections faster and less costly.

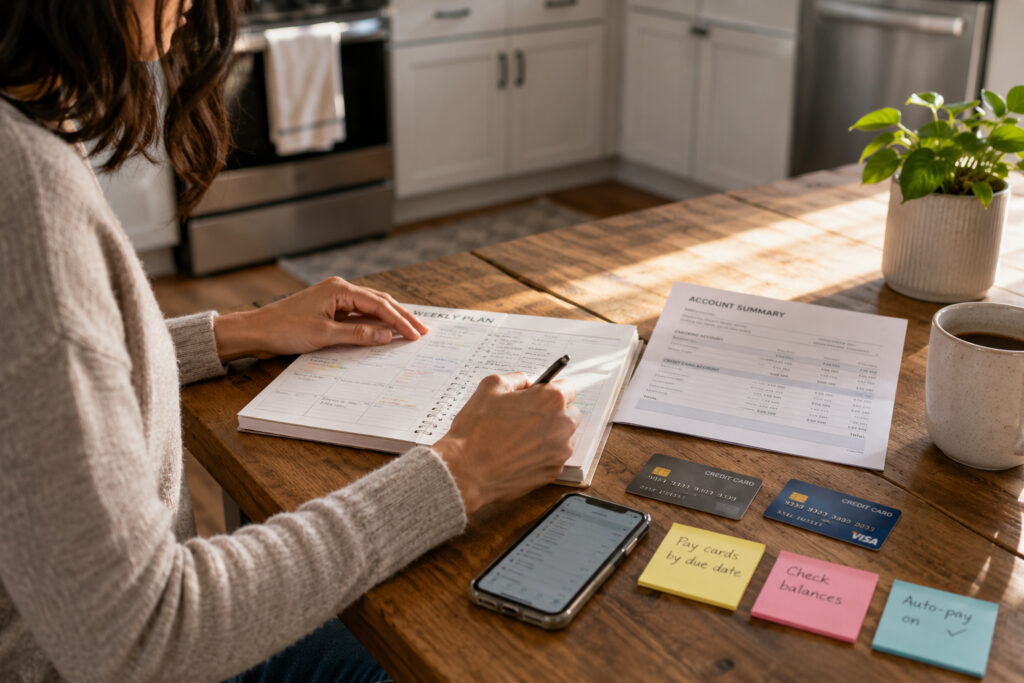

Adopt Reliable Payment and Utilization Habits

On-time payments and low credit utilization are two of the strongest drivers of score improvement. Aim to pay at least the minimum by the due date and, when possible, pay down balances before the statement closing date to lower reported utilization. Small, consistent overpayments — even $10 or $20 more than the minimum — shorten payoff timelines and reduce interest. These adjustments are simple to automate and maintain. Small behavioral shifts often yield visible changes in a few billing cycles.

Automating payments and setting calendar alerts remove friction and reduce missed payments. Over time, these modest changes build a positive repayment history.

Use Credit Tools and New Accounts Strategically

Adding a small, well-managed account or a secured card can diversify your credit mix and add positive trade lines. Only open accounts when they serve a clear purpose and you can commit to on-time payments. Monitor newly opened accounts carefully to avoid accidental overuse or unnecessary hard inquiries. Combining strategic new accounts with disciplined habits accelerates recovery safely. Be mindful of application timing to avoid clustering hard inquiries.

- Authorized user status on a long-standing account can help when used responsibly.

- Credit-builder loans or secured options create positive reporting without large limits.

Consider tools like credit-builder loans or becoming an authorized user on a reliable account when appropriate. Use them as complements, not substitutes, for consistent payment habits.

Conclusion

Micro-habits compound into measurable credit improvement when repeated reliably. Start small, track progress, and adjust priorities based on your snapshot. Over months, consistent steps create tangible, lasting change.