Small, consistent actions taken each week can make a meaningful difference in your credit profile over time. Focusing on short, manageable tasks reduces overwhelm and helps you stay disciplined without major changes to your routine. Weekly habits maintain momentum, prevent surprises, and gradually enhance the factors that influence credit records. This article outlines clear, practical steps you can adopt on a weekly basis to support stronger credit outcomes.

Why Weekly Habits Matter

Credit scoring is influenced by patterns, not isolated events, so frequent, small efforts compound into measurable improvement. Weekly check-ins let you catch billing errors, spot unusual account activity, and ensure on-time payments before they become problems. They also reinforce positive behaviors like controlled spending and proactive communication with creditors. By making credit maintenance a regular part of your schedule you reduce the risk of late payments and unplanned debt growth.

Establishing a weekly cadence creates a feedback loop that keeps financial goals visible and actionable. Over weeks and months, that visibility translates into strengthened payment histories and more stable utilization ratios. Consistency also builds confidence and reduces the likelihood of reactive, costly decisions.

Key Weekly Actions to Prioritize

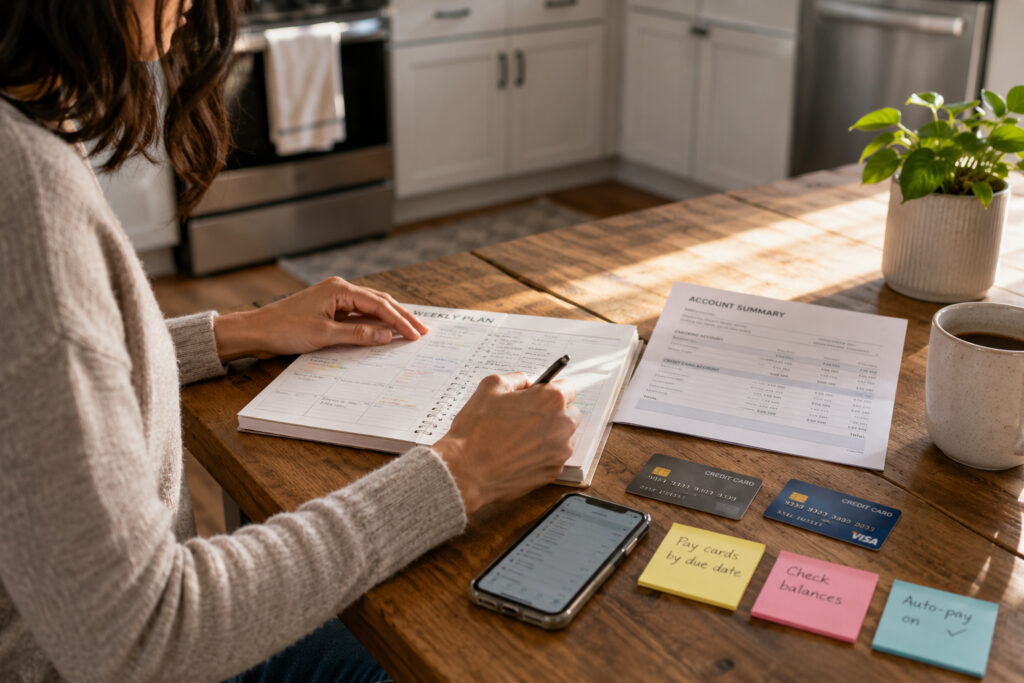

Start with a short financial review: check account balances, pending charges, and upcoming due dates to avoid surprises. Monitor credit utilization by noting card balances relative to limits and aim to keep utilization low across accounts. Verify recent transactions for errors or fraud and flag anything unfamiliar to resolve quickly with your issuer.

Combine these checks with a quick budgeting update to track progress against spending limits and savings goals. These small adjustments keep cash flow predictable and reduce the chance that you’ll miss payments or overspend. Over time, steady attention to these areas supports the score components that matter most.

Handling Common Setbacks

Even with good habits, setbacks like unexpected bills or an accidental late payment can occur; a weekly routine helps you respond faster. If you find a shortfall, prioritize resolving the outstanding balance and, when possible, contact the creditor to discuss options before the situation escalates. Document communications and keep follow-up reminders to ensure commitments are met and corrected on your accounts.

Use weekly reviews to assess whether any setback requires a temporary change to your routine, such as adjusting spending limits or creating an emergency buffer. These small course corrections prevent minor issues from becoming long-term problems.

Tracking Progress Without Overwhelm

Choose two or three simple metrics to track weekly, such as on-time payments, total utilization percentage, and the number of accounts with balances. Use a single spreadsheet or a free budgeting tool to record these metrics and visualize trends over time. Seeing steady improvements, even modest ones, reinforces the habit and keeps motivation high.

Finally, schedule a short weekly slot on your calendar dedicated to these checks so they become automatic. Over months, this low-effort practice yields clearer finances and stronger credit signals.

Conclusion

Adopting a few focused weekly habits creates steady momentum toward better credit health. Regular reviews, timely payments, and modest adjustments reduce risk and build positive patterns. Consistency wins: small weekly actions add up to meaningful long-term improvement.